GST on exports

CA Anand Singh | 08-May-2022

GST on exports

In exports, goods or services produced in the domestic country sold to persons residing in a foreign country. Governments encourage exports. Exports increase the foreign exchange reserves of the country. To make Indian products competitive in the international market, provisions of "zero-rated supply” introduced in GST for exports.

Making exports zero-rated means that the entire export transaction is tax-free. This means there is no need to pay tax either on inward supply or outward supply. Not only that also there is no restriction in Goods and Services Tax on claiming credit of taxes paid on input which used for providing such supply.

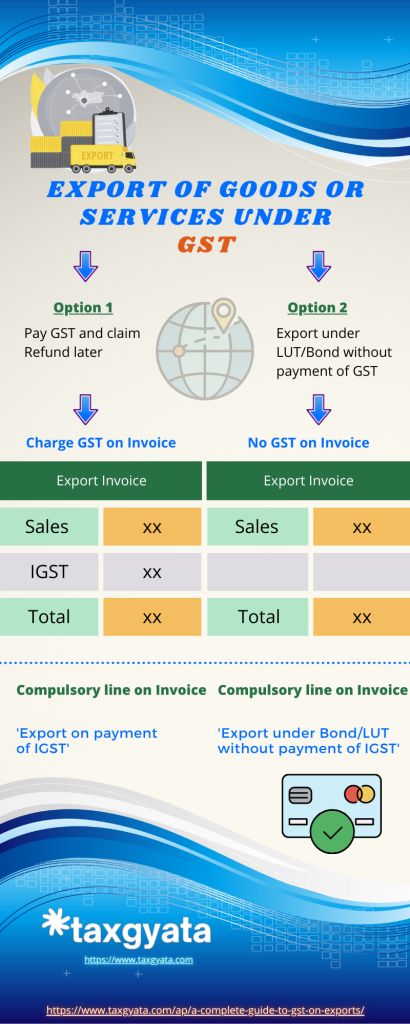

However, if GST is required to be paid on the export of goods or services at any point in time then a refund of the same can be claimed later or goods can be exported under bond/LUT without paying tax.

What is zero-rated supply in GST?

As per section 16(1) of the IGST Act, “zero-rated supply” means any of the following supplies of goods or services or both, namely:–

(a) export of goods or services or both; or

(b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

Meaning of export of goods in GST

Export of goods means taking goods out of India to a place outside India.

To qualify supply as export of goods, the only condition is that goods must move outside the country. If goods are supplied within India against the order received from a person residing in a foreign, such supply shall not be treated as export of goods.

Meaning of export of services in GST

Export of services means the supply of any service when, -

- The supplier of service is located in India;

- The recipient of service is located outside India;

- The place of service is outside India;

- The payment for such service has been received by the supplier of service in convertible foreign exchange; or in Indian rupees wherever permitted by RBI, and

- The supplier of service and the recipient of service are not merely establishments of a distinct person. if place of supply is out of India:

What documents are required for exports under GST?

The list of documents required to complete the export supply in GST is given in the below table:

|

Sr No. |

Document |

Description |

|

1 |

Import-export code (IEC) |

IEC is a 10 digit identification code issued by DGFT to import or export goods or services. |

|

2 |

Purchase order or service agreement as case may be |

A purchase order is an official document sent by the buyer to the exporter to confirm the description of goods, payment terms, delivery terms, etc. |

|

3 |

Export Invoice |

An export invoice is a billing document issued by the exporter which contains the same information as a GST invoice with certain additional information. |

|

4 |

Bond/LUT in case of export without payment of IGST |

A bond or letter of undertaking is a document filed by exporter to get exemption from IGST payment on exports. |

|

5 |

Shipping bill in case of export of goods |

A shipping bill is a document filed by the exporter with customs to move goods out of a country. |

|

6 |

Bank realization certificate (BRC) or foreign inward remittance in case of export of services |

BRC is a confirmation letter issued by banks to confirm that exporter has received payment against exports. |

Registration requirement for exporters under GST

Export of goods or services is treated as inter-state supply in GST. Accordingly, GST registration is compulsory for the exporter of goods under section 24 of the CGST Act, 2017. However, an exporter of services is not required to register for GST if his annual turnover is less than the exemption limit of Rs 20 lakh.

Documents required for registration:

Exporters need to upload the following documents while applying for registration on the Common portal.

- PAN card of exporter

- Aadhaar card of exporter

- Bank account documents

- Business address proof i.e. rent agreement or property tax receipt/electricity bill

- MOA, AOA, and certificate of incorporation in case of a company

- Partnership deed in case of a firm

Export invoice rules in GST

An export invoice is a billing document issued by the exporter which contains the same information as a GST compliant invoice with the following additional information.

- Compulsory mention that “Export on payment of IGST” or “Export under bond/LUT without payment of IGST”

- Name and billing address of the recipient

- Shipping address of the recipient (if the billing address and shipping address are not the same)

- Shipping bill detail

- Conversion rate from Indian currency to foreign currency

- The total value of the invoice both in terms of Indian currency as well as the foreign currency

- Date and number of ARE-1

What options are available for a refund of GST on exports?

As we mentioned above, exports in GST are tax-free. However, if tax is required to be paid on export supplies, any of the following two options can be exercised to claim a refund of the tax paid-

- Option 1: Pay integrated GST on the export of goods or services and later claim a refund of GST paid.

- Option 2: Export goods or services under bond or letter of undertaking without paying IGST and claim a refund of the accumulated input tax credit.

Applicability of GST on export freight

Entry number 19A and 19B of Notification No. 21/2019-Central Tax (Rate) provides GST exemption on “Services by way of transportation of goods by a vessel/aircraft from customs station of clearance in India to a place outside India” till 30th September 2020.

Further, Notification No. 04/2020-Central Tax (Rate) has extended this exemption till 30th September 2021.

Deemed exports under GST

Supply of goods notified under section 147 of the CGST act shall be treated as deemed exports. Such supplies shall be deemed as exports even goods do not actually move outside India. The intent, behind making specified supplies as deemed exports, is to reduce imports and outflow of foreign exchange from India. Conditions to qualify supply as deemed exports-

- Supply must be notified under section 147 of the CGST Act

- Goods must be manufactured in India

- Supply of goods only (not services)

- Supply must be done within India

- Consideration can be received either in Indian currency or foreign convertible currency

Notification No. 48/2017 – Central Tax dated 18 October 2017 has notified the following category of supply as deemed exports:

- Supply of goods against Advance Authorization

- Supply of Capital goods to Export Promotion Capital Goods Authorization (EPCG)

- Supply of Goods to Export Oriented Unit (EOU)

- Supply of gold by a bank or Public Sector Undertaking against Advance Authorization

Recent updates related to exports under GST

24 September 2021

Exporters shall undergo Aadhaar authentication for claiming a refund of tax paid on goods exported out of India. (Notification No. 35/2021–Central Tax)

Under Aadhar authentication, an authentication link is sent on the registered mobile number and email id. On clicking the verification link, a window for Aadhaar Authentication will open where an applicant needs to enter Aadhaar number and the OTP received on the mobile number linked with Aadhaar.

20 September 2021

CBIC clarifies that supply of services by a subsidiary/ sister concern/ group concern, etc. of a foreign company, which is incorporated in India under the Companies Act, 2013, to the establishments of the said foreign company located outside India (incorporated outside India), would not be barred by the condition (v) of the sub-section (6) of the section 2 of the IGST Act 2017 for being considered as export of services, as it would not be treated as supply between "merely establishments of distinct persons". (Circular No. 161/17/2021- GST)

Related

Export to Nepal and Bhutan under GST

Exports of both goods and services to Nepal and Bhutan are treated as ‘normal exports’, i.e. goods and services can be exported to Nepal and Bhutan under LUT.

GST refund on export of goods (With payment of tax)

Exporters are entitled to claim the refund of integrated tax (IGST) paid on goods supplied outside India. To claim a refund in the export of goods, the exporter does not require to file a separate refund application. Read more.

How to view submitted Letter of Undertaking (LUT) on the GST portal?

Steps to view submitted Letter of Undertaking (LUT). Access the GST Portal. Login to the GST Portal with valid credentials. Click to know complete procedure.